If you’ve been researching how to become an insurance adjuster, you’ve probably heard phrases like:

- “Wait until storm season.”

- “That’s when deployments happen.”

- “Storm season is when things get busy.”

But what does that actually mean? Does the industry shut down outside of storm season? Are there specific start and stop dates? Or is it something more complex?

For people new to the industry, “storm season” can sound like a mysterious window of opportunity, almost like the entire career revolves around a few chaotic months of the year. That confusion can lead to unrealistic expectations about income, stability, and how deployments actually work.

At AdjusterPro, we’ve helped over 100,000 students get licensed, and we’ve watched the ebb and flow of storms for over 20 years. While we provide training and licensing education, our goal isn’t to oversell the career or paint it as something it’s not. We want you to have an accurate picture so you can decide if this path makes sense for you.

In this article, we’ll break down:

- What “storm season” actually refers to and the major storm cycles in the U.S.

- What happens operationally when a major storm hits

- How adjusters get deployed

By the end, you’ll understand how storm season fits into the broader insurance ecosystem, and why it’s only one part of a much larger, year-round industry.

Table of Contents

- What Is “Storm Season” for Insurance Adjusters?

- When Is Storm Season in Adjusting?

- What Triggers Storm Deployments?

- How Do Adjusters Get Deployed After a Storm?

- Is Storm Season the Only Time Adjusters Work?

- Does Storm Season Mean More Income?

- Considering a Career in Independent Adjusting?

What Is “Storm Season” for Insurance Adjusters?

In simple terms, “storm season” refers to periods of the year when severe weather events are more likely to cause widespread insured damage. When a storm hits, independent adjusters need to be ready to deploy: it’s go-time.

It works like this: when large-scale weather events happen (hurricanes, hailstorms, fires, winter freezes), insurance carriers experience sudden spikes in claims. Those spikes create a surge in demand for adjusters.

Storm season isn’t a separate job or a different industry. And it doesn’t mean insurance adjusting only exists during certain months.

Instead, it refers to predictable periods when claim volume tends to increase due to weather-related events. Insurance claims happen year-round. Storm season simply refers to periods when the volume intensifies.

When Is Storm Season for Insurance Adjusting?

Traditionally in the US, “storm season” for adjusters refers to the Atlantic Hurricane Season (June–November).

While storms are unpredictable in severity, certain weather patterns are cyclical. These cycles influence when large-scale deployments are most common.

Traditionally, “storm season” refers to hurricane season, but there are other storm seasons that you should be familiar with as well.

1. Atlantic Hurricane Season (June–November)

- Primarily affects coastal and Gulf states

- Can create widespread wind and flood damage

- Often results in multi-state claim surges

- Deployments may last weeks or months

Hurricanes are among the largest drivers of catastrophe claims due to their geographic reach and severity.

Side Note: Pacific hurricane season technically runs May–November. The industry typically references the Atlantic season for U.S. impact.

2. Hail and Severe Thunderstorm Season (Spring–Summer)

- Common in the Midwest, South, and Plains states

- Primarily roof, siding, and exterior property damage

- Often regional but frequent

- Can occur in waves across multiple states

Unlike hurricanes, hailstorms may not dominate national headlines, but they generate significant claim volume every year.

3. Winter Storm Season (Late Fall–Winter)

Winter events often lead to both property damage and interior water losses, creating another surge in claim activity. Damage includes:

- Freeze claims

- Burst pipes

- Ice dams

- Roof collapses

Each of these storm cycles affects different regions and claim types, but they share one thing in common: They temporarily increase demand for adjusters.

What Triggers Insurance Adjusting Storm Deployments?

Storm response is a surge response system that insurance carriers rely on every year. Simply put, when a catastrophic storm hits, many people need to respond at once to handle the massive amount of claims.

The trigger is operational, not calendar-based. Insurance carriers monitor incoming claim volume carefully. When internal capacity can’t handle the workload, they bring in additional support through catastrophe (CAT) deployments.

In other words: More damage → More claims → More demand for adjusters.

Storm season increases the likelihood of that chain reaction, but the deployment itself is driven by real-time claim volume.

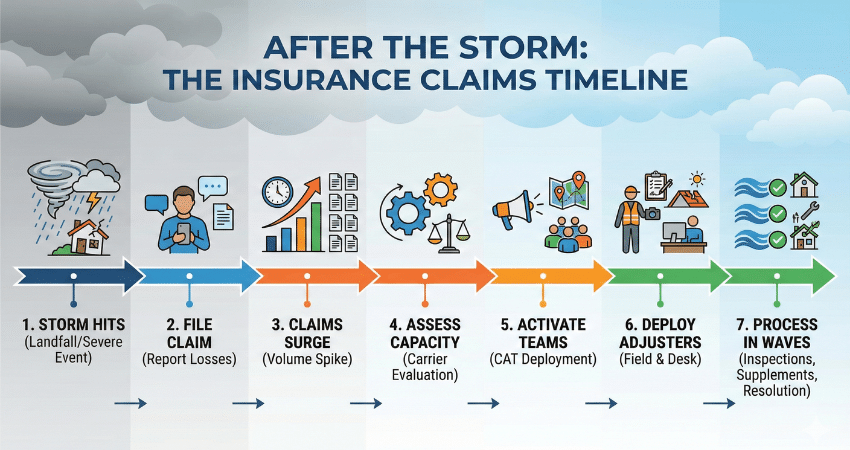

Here’s what typically happens:

| Steps + Action | Timeline Example (this can vary by circumstance, carrier, and location) |

| Step 1: Landfall or Severe Event Occurs: Weather systems move through an area and cause damage. | Hour 0 |

| Step 2: Claims Begin Filing: Homeowners and policyholders start reporting losses to their insurance carriers. | Within the first 24 hours |

| Step 3: Volume Spike: Claim intake jumps rapidly over hours or days. | Day 1 to Day 3 |

| Step 4: Carrier Capacity Assessment: Insurance companies evaluate whether internal staff can manage the workload. | Day 1 to Day 4 |

| Step 5: CAT Activation: Independent Adjusting (I.A.) Firms are notified. Deployment lists are created. | Day 2 to Day 5 |

| Step 6: Adjusters Deploy: Field adjusters travel to affected regions. Desk adjusters may handle remote claims. | Day 3 to Day 7 |

| Step 7: Claims Processed in Waves: Initial inspections occur first, followed by supplements, re-inspections, and ongoing adjustments. | Week 1 through several weeks or months |

How Do Insurance Adjusters Get Deployed After a Storm?

Adjusters don’t simply show up after a storm. Deployment depends on preparation, qualifications, and timing.

Before a storm ever happens, independent adjusters typically need to be positioned for deployment. That typically includes:

- Being on approved rosters with I.A. Firms

- Holding the proper state licenses for affected regions

- Completing any required carrier certifications or storm-specific training

Once a storm hits and claim volume begins to rise, firms usually contact adjusters in waves. Priority often goes to those who:

- Already hold the required licenses and certifications

- Have strong performance records

- Respond quickly

- Are immediately available to deploy

In the end, deployments are based on operational need and adjuster readiness. The more prepared and responsive an adjuster is, the more likely they are to get the call.

Is Storm Season the Only Time Insurance Adjusters Work?

No, this is a common misconception. In reality:

- Claims occur year-round.

- Storm season refers to surge periods.

- Deployments are event-driven.

- Some years are busier than others.

Storm season doesn’t create the insurance industry; it amplifies it. Understanding that distinction is important if you’re evaluating the career path realistically.

Does Storm Season Mean More Income for Adjusters?

Storm season plays a major role in the claims adjusting ecosystem, but it’s only one part of the bigger picture.

Insurance adjusting includes:

- Daily claims

- Desk adjusting

- Property inspections

- Re-inspections and supplements

- Auto and liability claims

- Non-weather-related losses

Storm events increase volume temporarily. They don’t define the entire profession.

Think of storm season as a surge cycle within a much larger system, one that operates every single day of the year.

Considering a Career in Independent Adjusting?

If you’re evaluating independent adjusting, confusing storm season with long-term stability can lead to unrealistic expectations about income and workload. Deployments are event-driven. Some years are busier than others. Success depends on preparation, not just waiting for the next storm.

If your bigger question is, “Is this a stable career path?” the next step is understanding what happens outside of surge events.

In “Is Independent Adjusting a Seasonal Job?”, we break down income consistency, workload patterns, and what the first few years really look like, so you can make a confident, informed decision.

Our goal is simple: give you the full picture so you can decide what’s right for you.