The laws that govern insurance, from licensing regulations and examinations to an insurance company’s obligations to its customers, are written in state constitutions as ‘statutes.’ Have you ever seen or tried reading a state statute? Let’s look at how our courses simplify insurance statutes, help you understand the material, and, most importantly, give you the knowledge to pass your adjuster exam.

Breaking Down Insurance Statutes

Take a look at this single sentence in a statute:

No cause of action in the nature of defamation, invasion of privacy, or negligence shall arise against any person for disclosing personal or privileged information in accordance with this Article, nor shall such a cause of action arise against any person for furnishing personal or privileged information to an insurance institution, agent, or insurance-support organization: Provided, however, this section shall provide no immunity for disclosing or furnishing false information with malice or willful intent to injure any person. [NC Gen Stat § 58-39-110 (2022)]

Say what?!

After reading it over a couple of times, maybe you can gather the gist of what this law is articulating. But it takes patience, a good vocabulary, and often, grammar knowledge to really understand what the lawyers were trying to say there. If asked, could you accurately simplify and summarize the information in that sentence? Here’s what we came up with:

“You can’t get in trouble with the law for sharing a customer’s personal information, as long as you only share information that the law says is okay to share (and where the law says it’s okay to share it). And remember, sharing false information with bad intentions will never be legal.“

That sounds better and is definitely easier to understand. But, so what? Why is statute 58-39-110 of North Carolina law relevant to you? Let’s dig in further.

Insurance Exam Content Outlines

That sentence is the third to last reference (out of 28 references) given under the fifth subtopic (out of 14 subtopics) of the last main topic (out of 7 main topics) on the North Carolina adjuster exam content outline. Did you get that? In other words, this is information you will need to know to pass the NC insurance adjuster exam. And it’s only a fraction of the information that NC has given you to study. Yikes.

But we aren’t just picking on North Carolina. For better or worse, the language in the statute above is the standard language used in every state’s book of laws. Most state exam content outlines include several references to state statutes that you’re expected to read, understand, and memorize.

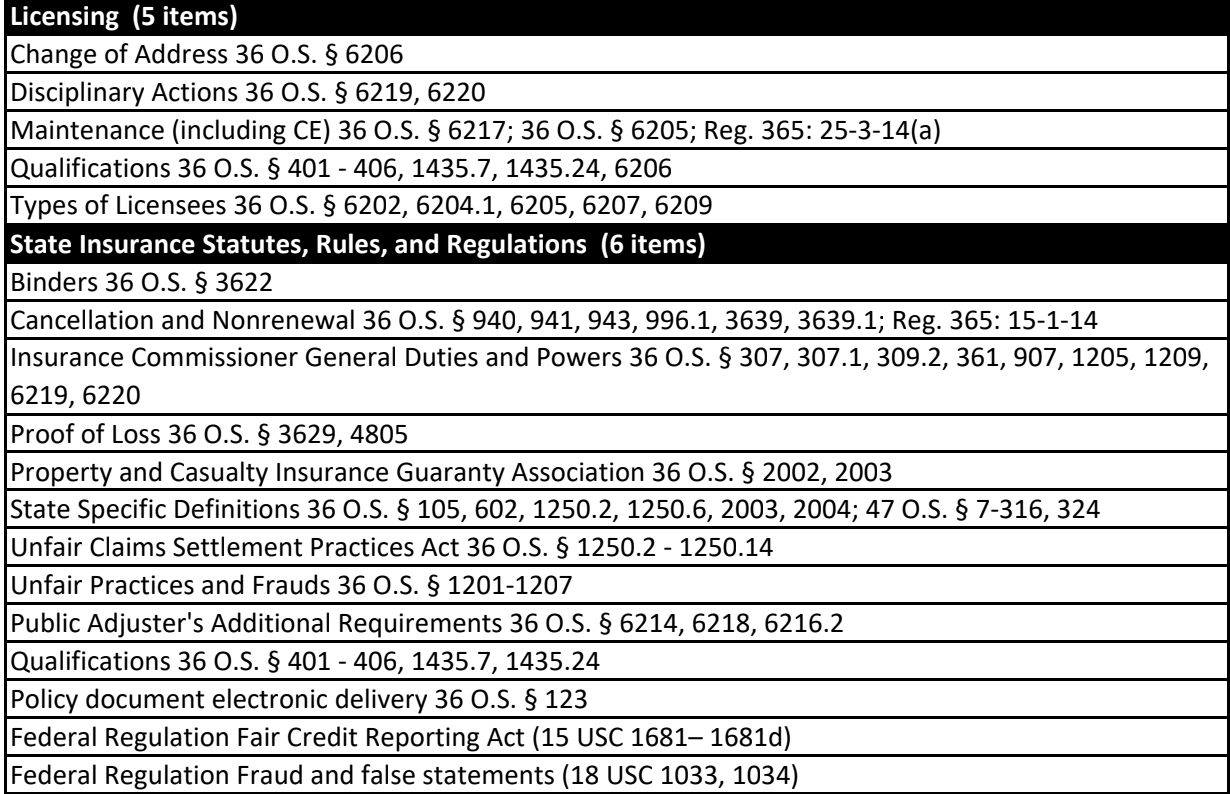

To give you an idea of how messy it can get, here’s a snapshot from the Oklahoma Property and Casualty Adjuster exam content outline (part of a 33-page PDF):

In the old days, this was all that was available if you wanted to study and learn the material for your insurance exam. Imagine doing what we did at the beginning of this article, but times 60. That’s a lot of statutes to read, understand, and memorize.

How AdjusterPro Courses Help You

When an AdjusterPro Course Development team sits down to write a course, like a North Carolina or Oklahoma Adjuster course, they begin by reading through the exam content outline released by the state (which is essentially your study guide).

After divvying up the work, each writer focuses on a specific portion of the outline and dedicates time and special attention to every topic and statute: studying it, doing outside research, and collaborating with experts when needed. Then, that writer takes the time to “translate” each statute into what I like to call “normal person speak.” In other words, they take the overly complicated legalese and turn it into language that a normal human could understand.

To give you a better idea of what this looks like, here are a couple more examples of how an AdjusterPro course writer interprets state statutes and then rewrites them so you, as the student, can understand and learn them. (Giving you the knowledge to ace your state exam!)

Hawaii state law:

The standard form fire insurance policy as authorized and in effect in the State of New York on December 31, 1943, or its approved equivalent, is established as the standard form fire insurance policy for this State, and no fire insurance policy shall be delivered or issued for delivery in this State in any other than the standard form or its approved equivalent with such additions or modifications as are allowed or required by this code. This section is not applicable to inland marine policies or policies written upon motor vehicles or aircraft. For the purpose of this section, “approved equivalent” means any form of policy which does not correspond to the standard fire insurance policy, provided that the coverage with respect to the peril of fire, when viewed in its entirety, is substantially equivalent to, or more favorable to the insured than that contained in the standard fire insurance policy and approved for use by the commissioner. [Beginning of HI Rev Stat § 431:10-210 (2023)]

AdjusterPro’s interpretation :

Hawaii has decided that its standard form fire insurance policy is the same as New York’s standard form. A Hawaii insurer is only allowed to use a different form if it’s equivalent to (or has better benefits than) the NY standard policy, and if the insurance commissioner approves it. Note that this rule does not apply to other types of insurance, like inland marine, motor vehicle, or aircraft policies.

Kentucky state law:

All claims arising under the terms of any contract of insurance shall be paid to the named insured person or health care provider not more than thirty (30) days from the date upon which notice and proof of claim, in the substance and form required by the terms of the policy, are furnished the insurer. [Beginning of KY Rev Stat § 304.12-235 (2022)]

AdjusterPro’s interpretation:

An insurer has 30 days to settle a claim after receiving proper notice and proof of loss.

Ultimately, our goal is to simplify statute language as much as possible, while making sure that the important information you need to know doesn’t get lost in translation.

Let’s go back to the state exam content outlines. You may have noticed that they don’t always include long lists of state statutes. For example, here’s a snapshot from the Texas Property and Casualty Adjuster Exam Outline:

Here, we have a completely different problem. There isn’t a statute in sight.

At first glance, Texas looks like it’ll be a lot easier to work with than Oklahoma. Who wants to spend hours finding and reading all those state laws? The problem with this outline, though, is that you’re not given any resources or references at all. This means that Texas expects you to research these topics on your own and then take a guess at which details, in which statutes you need to know about “TX residual markets” for the exam.

Often, state statutes still lurk behind these outline topics; you simply aren’t told which ones, leaving you to have to read through almost everything. For example, chapter 2151 of Texas’ Insurance Code talks all about one of its residual markets: the Automobile Insurance Plan, but the state outline didn’t tell you that.

AdjusterPro Courses Do the Work for You

When an AdjusterPro course writer encounters an exam topic with no statute references, that writer will work to find all the statutes on the topic, do additional outside research, read sample insurance policies, collaborate with team members, and consult experts. Then, the writer will compile and condense all the important information he or she learned into a neat and to-the-point explanation. Finally, every writer at AdjusterPro works with a reviewer so that no detail is missed or misinterpreted.

At the end of the writing process, the AdjusterPro writing team puts all of their research and writing together to produce a course on insurance adjusting that is specific to your state. Rest assured that the team always double-checks that they haven’t missed a single topic on the outline.

In addition to the main content, the writing team adds quizzes along the way so you can test your knowledge in real-time. Our courses also include practice exams with questions that are carefully crafted based on each topic. The practice exams mimic the way your state exam will be weighted according to the exam content outline. (Notice the percentage and number of questions on each topic in the Texas outline above.)

When studying for your adjuster exam using an AdjusterPro course, you don’t have to look up a single state statute. You don’t even have to look at the state exam outline if you don’t want to – we’ve done all of that for you. But if you’d like, you can study our course with your state outline next to you, checking off every topic as you go along.

Insurance regulation is a complicated business, made even more so by the way state laws are written. AdjusterPro courses simplify state insurance statutes so that you can actually understand and absorb the information. Not only will this help you pass the adjuster licensing exam, but it also means you’ll walk into your new career with the foundation to be a great insurance adjuster.

So, what are you waiting for? Let’s get studying!